First-Time Homebuyer Programs You Should Know About

First-Time Homebuyer Programs You Should Know About

Introduction

Buying your first home can feel like a marathon with no finish line—down payments, approvals, closing costs—it adds up fast. That’s why first-time homebuyer programs exist: to give you a leg up when entering the market.

Whether you’re planning to buy in six months or just getting started, understanding these programs can save you thousands of dollars and months of stress. Let’s break them down, one by one.

Why First-Time Buyer Programs Exist

Homeownership is a major wealth-building tool. But for many Canadians—especially younger buyers or those without family help—getting into the market feels out of reach.

Government-backed programs are designed to:

- Reduce upfront costs

- Make saving easier

- Lower taxes

- Ease lending barriers

- Level the playing field for new buyers

Used wisely, they can be the difference between “maybe someday” and “we got the keys.”

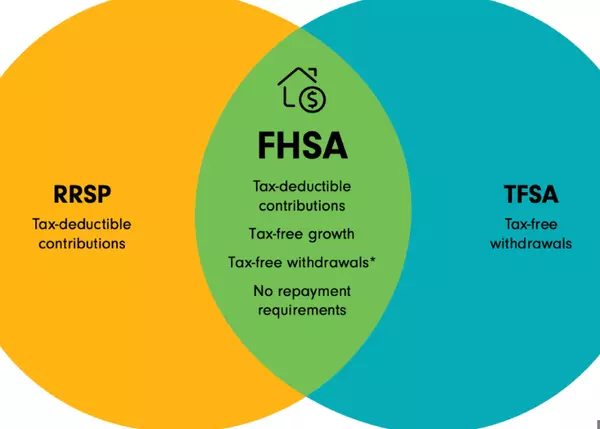

1. First Home Savings Account (FHSA)

How It Works

The FHSA is a new tax-advantaged savings tool that combines the best features of an RRSP and a TFSA.

- Contribute up to $8,000/year (max $40,000)

- Contributions are tax-deductible (like an RRSP)

- Withdrawals are tax-free if used for a qualifying home (like a TFSA)

Who Can Open One?

- Canadian resident, age 18–71

- First-time homebuyer (no home ownership in the past 4 years)

FHSA vs RRSP HBP

You can use both the FHSA and the Home Buyers’ Plan (covered below) for the same home—combining both gives you up to $100,000 in tax-advantaged savings.

2. Home Buyers’ Plan (HBP)

How to Use RRSPs for a Down Payment

The HBP lets you withdraw up to $60,000 from your RRSP to buy a qualifying home—tax-free. You must:

- Be a first-time homebuyer

- Use the home as your primary residence

- Repay the funds over 15 years

Repayment Rules

Each year, you're required to repay 1/15th of what you withdrew. If you miss a year’s repayment, that portion is added back to your taxable income.

Pro tip: Plan your payback strategy up front to avoid tax surprises.

3. First-Time Home Buyers’ Tax Credit

Eligibility Criteria

The federal Home Buyers’ Tax Credit (HBTC) offers a non-refundable credit worth up to $1,500. To qualify:

- You must be a first-time buyer

- You must move in within a year

- Your home must be eligible (most standard purchases qualify)

How to Claim It

- Claimed on your tax return

- Use Line 31270 (formerly Line 369)

- You and your spouse/common-law partner can split the credit

While it’s not a direct cash rebate, it helps offset closing costs like legal fees.

4. GST/HST New Housing Rebate

Qualifying Homes

If you buy a newly built home (or substantially renovate one), you may be eligible for a partial GST or HST rebate. The home must be:

- Your primary residence

- Below a certain price threshold (varies by province)

Claiming the Rebate

- Typically applied through your builder or lawyer during closing

- Or filed after closing if not claimed up front

This rebate can reduce costs by several thousand dollars, depending on your purchase price and province.

5. CMHC Insurance & First-Time Flexibility

Minimum Down Payment Rules

First-time buyers can purchase with as little as 5% down, thanks to mortgage insurance through CMHC (or similar providers).

Example: On a $400,000 home, that’s $20,000 down.

CMHC Benefits for First-Time Buyers

- Access to high-ratio mortgages

- Flexibility on income sources (especially for self-employed or gig workers)

- Newcomer programs for recent immigrants

While insurance adds to your monthly payment, it lets you buy with less cash up front.

6. Stacking Programs for Maximum Advantage

Real-Life Example

Let’s say you’re buying a $450,000 home:

- You use your FHSA to save $8,000/year (plus tax deductions)

- You withdraw $40,000 from your RRSP using the HBP

- You claim the $1,500 tax credit

- Your lender applies the GST rebate directly at closing

- You qualify for CMHC insurance, reducing the required down payment

Altogether, these tools can shave months or years off your buying timeline.

Timing Your Applications

Some programs require upfront setup (like the FHSA), while others apply during taxes or after purchase. Working with a professional helps you sequence everything correctly.

7. Municipal and Local Incentives

What to Ask Your Realtor or City

- Are there first-time buyer grants in my city?

- Are there renovation or energy-efficiency rebates?

- Is there affordable housing or down payment assistance?

Examples of Past Local Programs

- Saskatoon previously offered tax abatements for new builds in select areas

- Some municipalities offer energy retrofit grants tied to CMHC loans

- Non-profits like Habitat for Humanity provide shared-equity ownership programs

These fly under the radar, so don’t assume you're not eligible—ask.

Common Misconceptions About First-Time Programs

- ❌ “I make too much money to qualify.”

✅ Most programs aren’t income-tested (especially FHSA/HBP). - ❌ “You can only use one program.”

✅ Many are stackable and meant to be used together. - ❌ “I’ll have to pay everything back with interest.”

✅ HBP and FHSA are repayment-free if used properly.

Should You Use a Mortgage Broker?

If you’re juggling programs, lenders, and deadlines—it’s a lot. A mortgage broker can help:

- Navigate lender requirements

- Combine programs for max advantage

- Access alternative financing if needed

Think of them as your home financing GPS.

Final Thoughts: Empowering First-Time Buyers

Homeownership may feel out of reach, but these programs were built to bridge the gap. With the right knowledge—and the right team—you can confidently take the next step toward owning a home.

Start small. Save smart. Ask questions. And stack the tools in your favour.

FAQs

1. Can I use both the FHSA and the HBP at the same time?

Yes! You can combine both programs to supercharge your down payment savings.

2. Do I have to repay the FHSA funds like I do with HBP?

No. FHSA withdrawals are tax-free and don’t need to be repaid, as long as they’re used for a qualifying home.

3. What qualifies me as a first-time buyer?

Generally, you must not have owned a home in the last 4 years. Each program may define this slightly differently, so read the fine print.

4. Is there a deadline to repay HBP withdrawals?

Yes. You must start repaying in the second year after withdrawal and finish over 15 years.

5. Can I still get help if my credit score isn’t great?

Yes. Some programs are more flexible, and a broker can help find lenders who work with alternative income or lower credit.

Categories

Recent Posts

GET MORE INFORMATION